It shows the changes in chart of the past 14 days.

Average true range indicator calculation.

Wilder used a 14 day atr to explain the concept.

Average true range atr is a volatility indicator that shows how much an asset moves on average during a given time frame.

For this example the atr will be based on daily data.

Calculation typically the average true range atr is based on 14 periods and can be calculated on an intraday daily weekly or monthly basis.

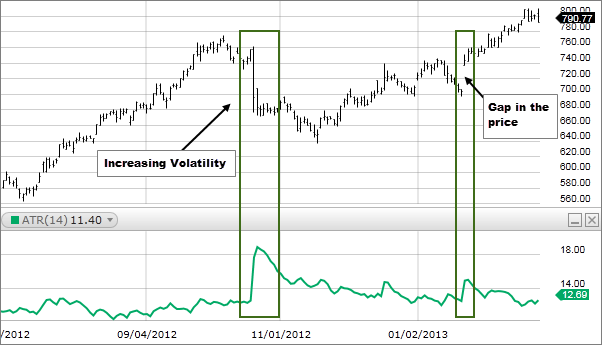

Remember that the atr calculates only the historical volatility and that it can t predict the future.

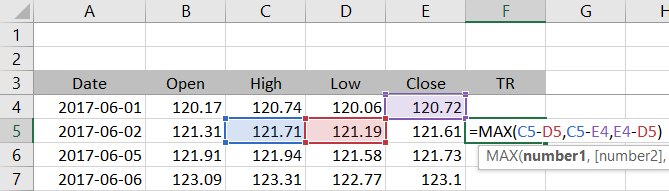

Calculating average true range atr in excel this is a detailed guide to calculating average true range atr in excel.

We will first calculate true range and then atr as moving average of true range.

The average true range is an n period smoothed moving average smma of the true range values.

In theaverage true range indicator the ups and downs in value shown in the upper right corner in the window.

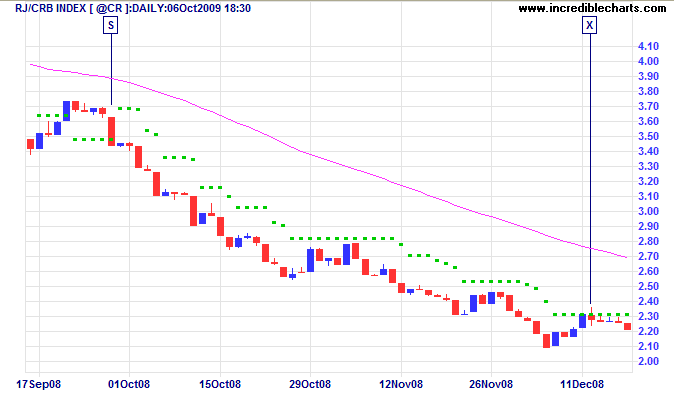

For commodity market analysis.

We will do all the three popular atr calculation methods simple exponential and the original wilder s smoothing method.

The indicator does not provide an indication of price trend simply the degree of price volatility.

So the average true rangeindicator calculates the numbers and prepares planning for making a decision.

Traders can use shorter or longer timeframes based on their trading.

For example when calculating the average true range for a 14 day period you would take the average of the true ranges over 14 days.

The average true range atr is an exponential moving average of the true range.

It was developed by j.

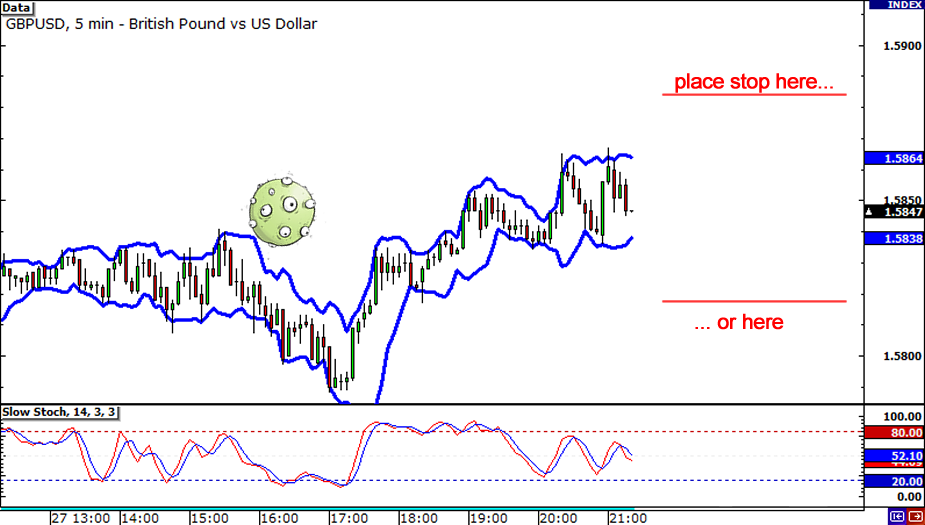

Atr to calculate the stop loss every time you are choosing your entry size you need to take into account the price volatility.

It is typically derived from the 14 day moving average of a series of true range indicators.

Average true range atr is a technical indicator measuring market volatility.

Theaverage true range is the set of 14 days.

Average true range is a technical analysis indicator that measures the price change volatility.

The indicator can help day traders confirm when they might want to initiate a trade and it can be used to determine the placement of a stop loss order.

In order to calculate the average true range you take the average of each true range value over a fixed period of time.

Average true range atr is a technical analysis volatility indicator originally developed by j.

The indicator says nothing about trend strength or direction.

/ATR-5c535f8fc9e77c000102b6b1.png)